The obscenity of executive pay at the time was still relatively new and it was awesome to hear him talk about the issue. Now executive comp is an old obscenity, like a grandmother's curse. "Feh!"

Even in our topsy turvy world, it seems that the one thing everyone can agree on is paying themselves raises with other people's money. It is certainly the one issue on which all our government representatives tend to agree. All the more reason to continue to shed light on the practice.

For smaller companies, I typically see Board cash pay in the $10k-$25k range and a few thousand shares. Occasionally you see Boards putting skin in the game, though no examples come to mind at the moment.

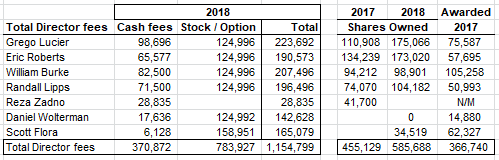

Invuity's latest proxy demonstrates the wrong side of comp, a greedy, do nothing board paying itself an absurd fee justified by nothing. Here is the board comp for $75M market cap company trading at its 52-week lows, whose stock is down 65% over the last 52-weeks, 50% ytd and whose new CEO is trying to talk up better capital allocation to the street.

I'm sure Boards justify these things using comparables but the aspect of benchmarking everyone seems to forgets is adjusting plus / minus from the baseline depending on performance. So I'd be fine with them using a benchmark, just deduct 65%. Oh and by the way, granting oneself $125K worth of shares is not a form of alignment.

Here's the cash comp they intend to pay themselves next year, roughly the same as last year. That the Chairman takes a small cut infers he knows it's excessive, but the cutback isn't nearly sufficient.

The company reports quarterly earnings in a few days and based on the stock's recent performance, I guess the market expects 1Q18 sales below consensus $9.5M and / or management will lower already conservative guidance of 5% topline growth.

It would be pretty dramatic if this happens on top of plenty of drama year to date: The new CEO was announced in mid-February and there was an equity raise in March.

Whatever happens, the new CEO will have to articulate a lucid and reasonable plan, and I expect he will. As I see it, the reasons for owning the company haven't changed much: Great product, selling okay, scaling the marketing curve, with optionality to do much better under better management, and with the whole company selling for less than 2x sales.

Here we are under ostensibly better management and I have been trying to keep my head about even as the stock slides and the anonymous comments pile up on CafePharma. Obviously, I think investors will get paid or else why would I own this, but I think the aspects that I underweighted in my initial analysis, notably the prior CEO's spending ways and the excessive Board comp, takes on increasing weight under the new CEO, and I just keep thinking "The Board should contribute not detract from the new CEO's efforts by making material changes to their comp." I recommend a few changes in the letter I sent today.

***

Dear Chairman:

I was shocked and disappointed to open my Invuity proxy and observe continued excessive Board compensation.

What you pay yourselves even as you’ve overseen significant and material destruction of shareholder value should outrage Invuity’s employees and customers from whom you are effectively taking much needed resources. Furthermore, the extent at which you sell shares and the miserliness with which you personally buy them should outrage shareholders, the majority of whom have lost money on this investment to date.

No doubt, a compensation structure that exists only to enrich yourselves fit comfortably with the norms, cultures and behaviors of the prior CEO, but this has no place in the current strategy of managing capital more efficiently and effectively.

We have a new CEO who is working hard to improve so much prior mismanagement that occurred under your watch and that resulted in the evaporation of capital market credibility. The Board can help him re-establish credibility by following a sane and reasonable compensation structure.

I recommend the following two steps to show faith and confidence in his efforts and in the company in general:

• Take no compensation until the firm starts earning money.

• Buy shares with your own personal money until the Board effectively owns 20% of the company.

Lead by example. Stop this senseless self-enrichment. It will do right by your employees, customers and shareholders and it will materially and beneficially contribute to the company’s new efforts towards a wiser and smarter approach to capital allocation.

Sincerely

-- END --

ALL RIGHTS RESERVED. PAST HISTORY IS NO GUARANTEE OF PRIOR RETURNS. THIS IS NOT A SOLICITATION FOR BUSINESS NOR A RECOMMENDATION TO BUY OR SELL SECURITIES. I HAVE NO ASSURANCES THAT INFORMATION IS CORRECT NOR DO I HAVE ANY OBLIGATION TO UPDATE READERS ON ANY CHANGES TO AN INVESTMENT THESIS IN THE COMPANIES MENTIONED HERE, WHICH I MAY OWN.